Black-Scholes model was developed by Fischer Black and Myron

Scholes in 1973. It is a mathematical

model of a financial market containing derivative investment instruments (Read more here). It is widely used, often with adjustments, to

determine the price of options.

There are many types of derivative options in the

market. One of the most popular

derivative options in Bursa Malaysia are the Structured Warrants (Read

more here). Today, I am going to

discuss the usage of Black-Scholes model in Structured Warrants evaluation.

To construct a simple Black-Scholes model using excel, one

can refer to this link. I did some modification on the model in order

to fit the characteristics of the structured warrants available in Bursa

Malaysia.

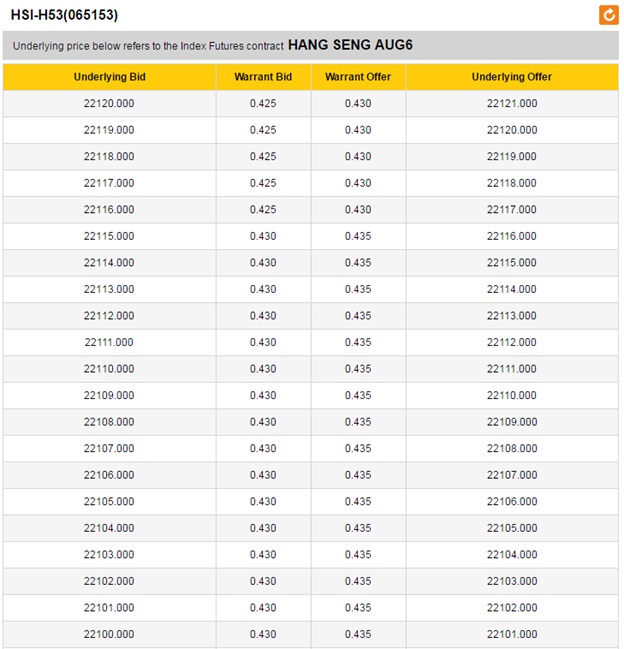

The following table (Table 1) is the structured warrants

price of the HSI-H53 as at 26-Jul-16. To

check the accuracy of the model, it is compared with the offer price by the

issuer (Table 2). This model was tested

on other structured warrants as well; the accuracy is always within the spread

of the structured warrants.

Table 1

|

Future Index

|

Black-Scholes Model

HSI-H53 price

|

|

22120

|

0.429

|

|

22110

|

0.431

|

|

22100

|

0.432

|

|

21880

|

0.433

|

Table 2

The following snapshot (Picture 1), is the Black-Scholes

model in excel format. (Readers who are interested to construct the

Black-Scholes model using Excel spreadsheet can contact me via email. Private tutorial or class can be arranged.)

Picture 1

There are few variables that affect the structured warrant

price. The most significant factor is

the underlying stock price. In this

example, it is the Hang Seng Future Index.

The following table (Table 3) shows the impact of Hang Seng Future Index

changes to the HSI-H53 price. Every 1%

changes of the Hang Seng Index with cause the HSI-H53 price to fluctuate about

6%.

Table 3

|

Future Index

|

Put Option Price

|

Percentage changes of

Index

|

Percentage changes of Put

Option Price

|

|

23205

|

0.313862973

|

5.00%

|

-27.31%

|

|

22984

|

0.334834542

|

4.00%

|

-22.46%

|

|

22763

|

0.357055027

|

3.00%

|

-17.31%

|

|

22542

|

0.380583676

|

2.00%

|

-11.86%

|

|

22321

|

0.40548107

|

1.00%

|

-6.10%

|

|

22100

|

0.431809

|

0%

|

0%

|

|

21879

|

0.459630311

|

-1.00%

|

6.44%

|

|

21658

|

0.489008773

|

-2.00%

|

13.25%

|

|

21437

|

0.520008864

|

-3.00%

|

20.43%

|

|

21216

|

0.552695579

|

-4.00%

|

28.00%

|

|

20995

|

0.587134208

|

-5.00%

|

35.97%

|

The second significant factor that will impact the option

price is the holding period. In option

trading, “buy and hold” strategy is “No”, “No”, “No”. Because it is very important, so have to say

it three times. The following table

(Table 4) shows the holding period impact of the put option.

Table 4

|

Hang Seng Future Index

|

Holding Duration

|

Warrant Price

|

%

|

|

22100

|

0

|

0.431

|

0

|

|

22100

|

3

|

0.422

|

-2.09%

|

|

22100

|

5

|

0.416

|

-3.48%

|

|

22100

|

10

|

0.399

|

-7.42%

|

|

22100

|

14

|

0.386

|

-10.44%

|

From the table we can see that, even the underlying Hang

Seng Future Index stays constant, by holding the put option for 3 days, the

option price will automatically reduce by 2.09%. As such, in side way market, where the Index

stay about the same level for long period of time, eventually the option price

will diminish to zero value.

There is another important variable in Black-Scholes model,

which is the implied volatility. This is

the most difficult variable to determine.

There are many ways to estimate but for now, the easiest way is to use

the implied volatility rate provided by the structured warrants issuer.

In summary, traders who are interested in structured warrants trading can use the Black-Scholes model to evaluate the risk and

return. The key principle is – Do not

apply “buy and hold” strategy on option trading. Unless the option is deep in the money and

the trader is ready to exercise the option on maturity. That will be discussed in another article.

Disclaimer: The above option

price calculations do not imply any buy or sell recommendation. The author disclaims all liabilities arising

from any use of the information contained in this article.